Latest News Archive

Please select Category, Year, and then Month to display items

20 August 2025

|

Story Dr Annelize Oosthuizen

|

Photo Supplied

Dr Annelize Oosthuizen, Subject Head of Taxation in the School of Accountancy, University of the Free State.

Dr Annelize Oosthuizen, Subject Head of Taxation in the School of Accountancy, University of the Free State.

With the two-pot retirement system having been effective from 1 September 2024, it is important to demystify certain aspects to prevent an unpleasant surprise when you retire. Although there are other complex rules, this article was simplified and does not deal with exceptions. It also does not deal with members of a provident fund who were 55 years of age or older on 1 March 2021. Furthermore, reference to retirement funds is to a pension fund, provident fund or a retirement annuity fund (a discussion on preservation funds is therefore excluded).

Three, not two pots

Firstly, there are effectively three pots and not two.

- The first pot is referred to as the vested component. You will only have this component if you were a member of a retirement fund prior to 1 September 2024. This component consists of the member’s interest (balance) in the retirement fund on 31 August 2024 (the day before the implementation of the two-pot system) after being reduced with the amount of the seed capital that was transferred to the savings pot (see below). This seed capital amount was calculated as the lesser of 10% of the value of the member’s interest in the fund on 31 August 2024 or R30 000. No further contributions will be allocated to this component from 1 September 2024. Upon retirement, one-third of the funds in this component can be taken in the form of a lump sum. The balance will be transferred to the retirement component below and will be paid out in the form of monthly annuities.

- The second pot is the savings component. The opening balance of the savings component is the seed capital that was transferred from the vested component above. Thereafter, from 1 September 2024, one third of your monthly contributions to the retirement fund are allocated to this component.

- The third pot is the retirement component. From 1 September 2024, two-thirds of your monthly contributions to the retirement fund are allocated to this component. The funds in this component can only be accessed upon retirement (i.e. after reaching your retirement age, which is stipulated in the fund rules). Furthermore, upon retirement, the money in this pot is only paid out in the form of monthly annuities (i.e. monthly pensions) and no lump sum can be taken from this pot unless its total value is R165 000 or less.

Withdrawals are taxed unfavourably

Secondly, withdrawing from the savings component before retirement has adverse tax implications.

- From 1 September 2024 onwards, one is allowed to make an annual withdrawal (minimum of R2 000) from the savings component even if you have not yet reached your retirement age and although you are still employed. It is, however, important to remember that such withdrawals are taxed very unfavourably since they are taxed by using the normal progressive tax tables that apply to your other income such as salary. If you wait for your retirement and only withdraw from this savings component upon retirement, the first R550 000 will be tax-free and withdrawals above R550 000 will be taxed at rates much lower than the current progressive tax rates applicable to other income.

- Upon retirement, only the money in the savings component is allowed to be taken as a lump sum. If you therefore withdraw all the money from this pot annually prior to retirement, you will not have any funds available to access as a lump sum on retirement and will only have access to the monthly annuities payable from your retirement component.

Less funds available

Lastly, for those members who have a vested component (i.e. who became members of the retirement fund before 1 September 2024), the old rules still apply to the funds in that component. Therefore, upon retirement, you will still be able to take one third of the value of your vested component as a lump sum. The balance will be transferred to the retirement pot and will be paid out in the form of monthly annuities.

To summarise, even though it might appear lucrative to withdraw from your savings component annually, it is advised that you refrain from doing it unless you really need the funds to fulfill basic needs. Withdrawing prior to retirement has the following adverse consequences:

- Money withdrawn from the savings component is taxed at higher rates than what would have applied had you reached your retirement age and retired. You will therefore not make use of the R550 000 tax-free option.

- You will have less funds available to pay out as a lump sum on retirement. As a simple calculation, had you not withdrawn R30 000 in a single year, conservatively calculated at a rate of 5%, this R30 000 would have grown to R79 599 (R139 829 if a rate of 8% is used) calculated over 20 years that can be withdrawn tax-free when utilising the R550 000 tax-free portion on retirement.

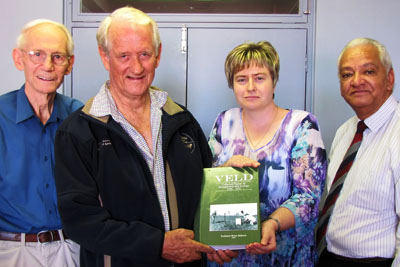

UFS receives exclusive copy of Pasture Science research volume

2010-04-22

|

From the left are: Dr Malcolm Hensley (Soil, Crop and Climate Sciences, UFS), Prof. Brian Roberts, Ms Cathy Giesekke (UFS Sasol Library) and Prof. Neil Heideman (Acting Dean: Natural and Agricultural Sciences, UFS).

Photo: Lize du Plessis |

The University of the Free State (UFS) became the proud recipient of a copy of a Pasture Science research volume.

The 508-page volume was presented by Prof. Brian Roberts, an adjunct professor at the James Cook University in Cairns, Australia, to the UFS Sasol Library. It consists of 43 papers on his agricultural research work in the Free State from 1956 to 1975.

He said the Faculty of Natural and Agricultural Sciences at the UFS had the power and expertise to lead the way in food security in South Africa and in building a sustainable society. He also stated that not enough people were taking food security seriously.

“Whatever else you regard as priority, none is more basic than support for the nation’s food producers,” he said.

The papers in the bound copy are arranged in two groups. The first section focuses on Pasture Management. “This series forms a useful overview of Pasture Science,” he said.

The section on Grassland Science covers all aspects of the maintenance, improvement and utilisation of veld and cultivated grasslands.

The second part is a series of publications arising from his fieldwork in the Free State, Eastern Cape and Lesotho.

“Having read with great interest the curriculum vitae of the Vice-Chancellor of the UFS, I felt a strong inclination to contribute somehow to the transformation process and the emerging future UFS,” said Prof Roberts.

Although he acknowledged that change could not happen overnight he was, however, positive that medium-term results could be achieved in that regard.

“One way of doing this is to focus staff and students’ attention on working towards a sustainable society, an on-going curriculum challenge which should, at an early date, replace the past preoccupation with race – an issue that has dogged progress for too long,” he said.

Prof. Roberts was a foundation lecturer in Pasture Science at the UFS 36 years ago before he left for Australia where he plays a fundamental role in land-use planning.

He is also recognised as the father of Landcare, an Australian partnership between the community, government and business to protect and repair the environment.

Media Release

Issued by: Mangaliso Radebe

Assistant Director: Media Liaison

Tel: 051 401 2828

Cell: 078 460 3320

E-mail: radebemt@ufs.ac.za

21 April 2010